Corporate Internet Banking in 2025: APIs, H2H, ERP & Cloud Integration Explained

As businesses scale and become more digitally mature, Corporate Internet Banking (CIB) is no longer just about viewing balances and initiating NEFT payments—it’s about real-time automation, deep ERP integration, cloud-first infrastructure, and intelligent reconciliation. This blog demystifies how modern CIB works and how it integrates seamlessly with systems like Tally Cloud, Zoho Books, SAP, and Oracle through APIs and Host-to-Host (H2H) connections.

What is Corporate Internet Banking (CIB)?

Corporate Internet Banking (CIB) is a secure digital platform offered by banks to help businesses manage bulk payments, collections, cash flows, reconciliations, tax payments, and more, without visiting a branch. With increasing adoption of automation, CIB is now integrated directly into a company’s accounting and ERP systems.

Key Integration Models in CIB

Today’s CIB platforms support two major models of integration:

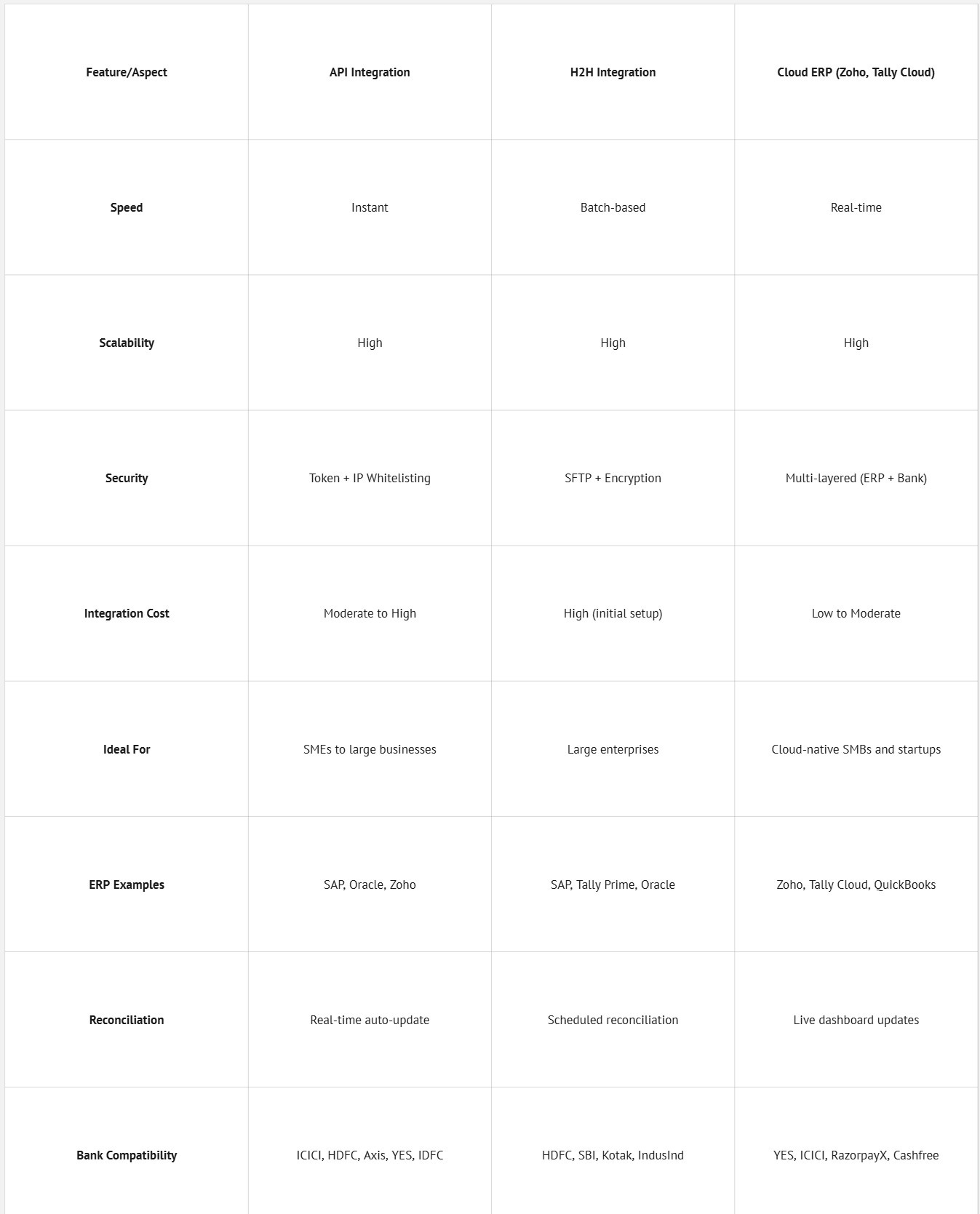

1. API Integration

Real-time connection between ERP (e.g., Zoho, SAP, Oracle) and bank systems.

Highly dynamic, event-based, and instant.

Ideal for growing businesses with frequent transactions.

2. Host-to-Host (H2H) Integration

File-based exchange between ERP and the bank using secure SFTP or VPN tunnels.

Designed for batch processing and high transaction volumes.

Used by large enterprises with predictable payment cycles.

Cloud-First Architecture: Modern CIB Infrastructure

Modern integration isn't possible without cloud-backed infrastructure. Here's how the pieces come together:

How It All Works: End-to-End Process

Step 1: Transaction Creation

User creates invoices or selects vendors inside ERP (Tally Cloud, Zoho, SAP).

Step 2: Instruction Dispatch

In API setup: Payment request is sent instantly to the bank via API.

In H2H setup: A file is auto-generated and sent via SFTP to the bank.

Step 3: Bank Processing

A bank verifies credentials, checks approvals (e.g., maker-checker), and initiates the fund transfer.

Step 4: Response to ERP

Bank sends back transaction status, UTR, or rejection reason.

ERP updates payment ledger, reconciles status, and logs the activity.

Real-World Use Case

A mid-sized NBFC using Zoho Books (cloud-based) integrates with YES Bank APIs via middleware like Cashfree or RazorpayX.

Finance team schedules payments from Zoho → Payment request hits the bank API → YES Bank processes payment instantly → Zoho updates UTR and closes the invoice — all in seconds.

Comparison Table: API vs H2H vs Cloud-Native ERP

Security Measures in Place

Encryption: TLS, SSL, or SFTP encryption ensures safe data transfer.

Token Authentication: For API access and role-based access control.

Maker-Checker: Dual or multi-level approvals for large-value transactions.

Audit Trails: Logs maintained at ERP, middleware, and bank levels.

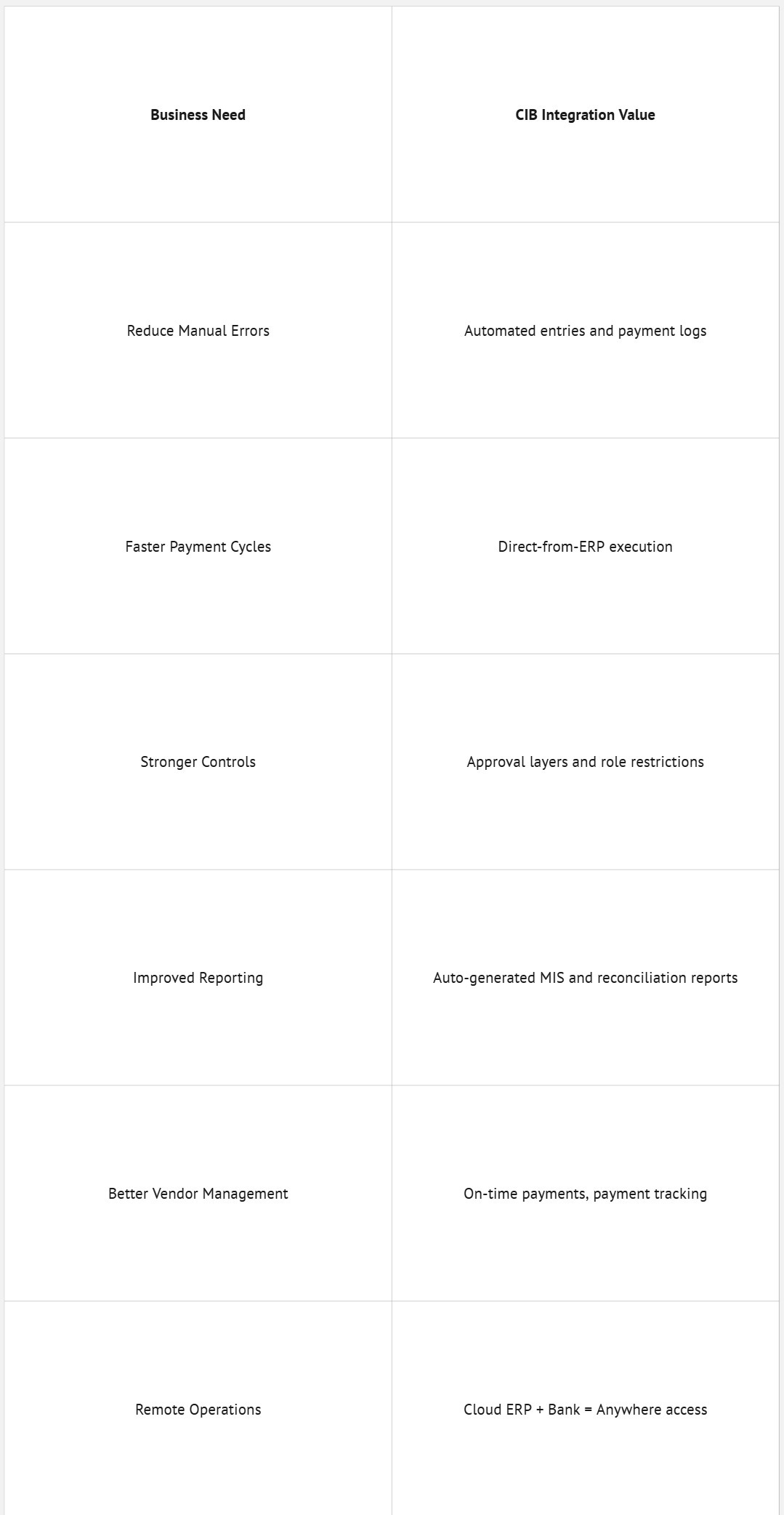

Why Should Businesses Care?

✅ Final Thoughts

The shift to API-driven, cloud-enabled, and ERP-connected Corporate Internet Banking is not just a technology upgrade—it’s a strategic necessity. Whether you’re an NBFC, fintech, manufacturer, or logistics provider, integrating your financial systems with banks can drastically reduce overhead, enhance accuracy, and provide greater financial control.