Understanding the Difference Between Banks and NBFCs

In India’s evolving financial ecosystem, both Banks and Non-Banking Financial Companies (NBFCs) play pivotal roles in driving credit access, financial inclusion, and economic growth. Yet, their functions, regulations, and operational boundaries are quite distinct. Let’s break down the key differences between the two.

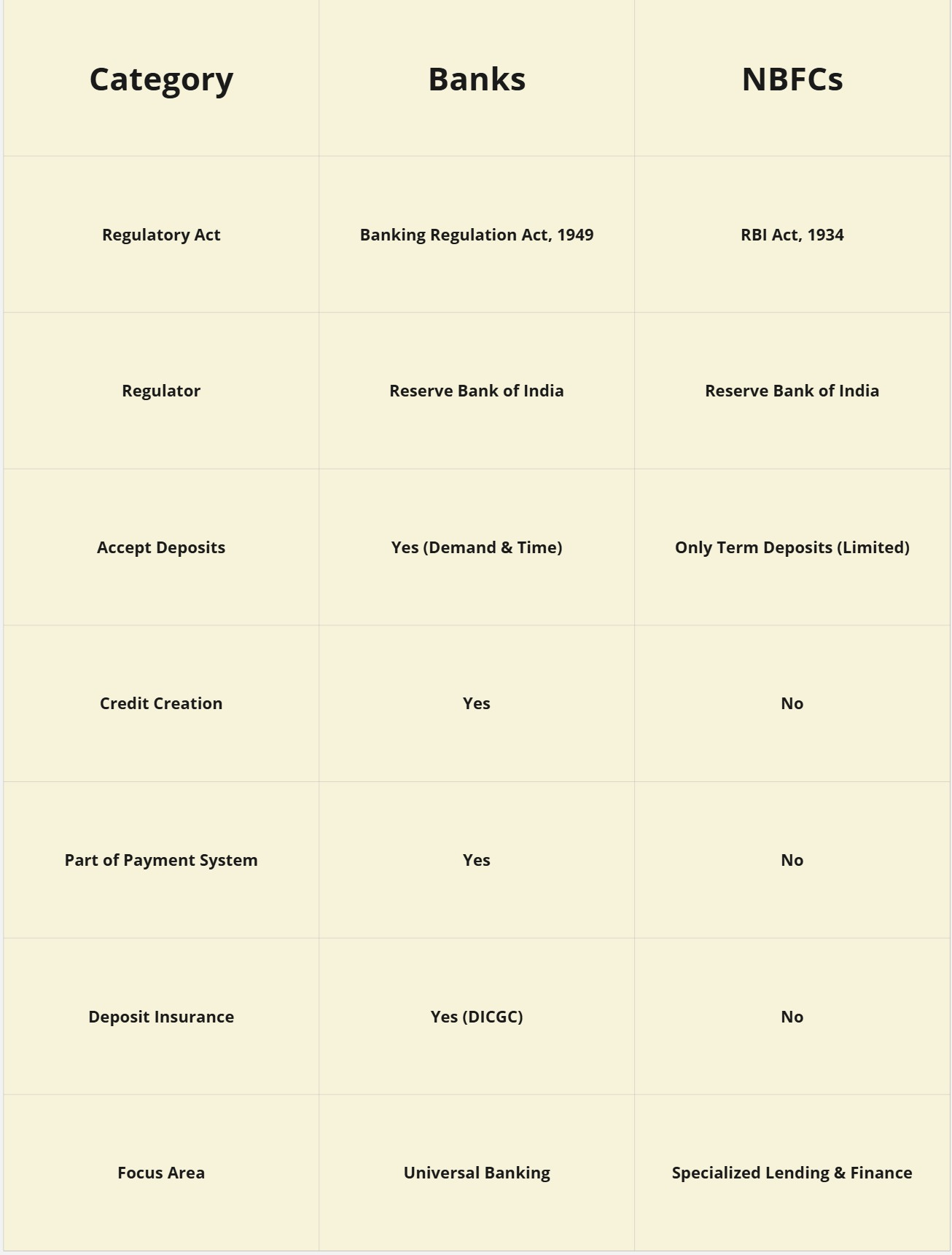

1. Regulatory Framework

Banks operate under the Banking Regulation Act, 1949 and are tightly supervised by the Reserve Bank of India (RBI). They are integral to the country’s monetary system and are allowed to create credit.

On the other hand, NBFCs are governed by the RBI Act, 1934. While they are also under RBI oversight, their compliance requirements are lighter, allowing them more operational flexibility.

2. Core Functions

Banks provide a wide range of financial services — from accepting deposits and offering loans to facilitating digital payments and international remittances.

NBFCs, in contrast, specialize in lending, asset financing, leasing, hire purchase, and investment activities, often catering to customer segments underserved by banks.

3. Deposit Acceptance

A major differentiator is deposit-taking capability.

Banks can accept both demand deposits (like savings or current accounts) and time deposits (like fixed deposits).

NBFCs, however, cannot accept demand deposits. Only a limited number of NBFCs, classified as Deposit-taking NBFCs (NBFC-D), can accept term deposits under strict RBI norms.

4. Credit Creation

Banks create credit by lending a portion of the deposits they hold — an essential function for liquidity and monetary supply in the economy.

NBFCs do not create credit in this manner; they primarily depend on borrowings, market instruments, and capital infusions to fund their lending operations.

5. Payment and Settlement Systems

Banks are part of the payment and settlement ecosystem, offering services like UPI, NEFT, RTGS, and IMPS.

NBFCs are not allowed to operate payment systems directly — though many partner with banks and fintechs to deliver payment-linked solutions.

6. Deposit Insurance

Deposits in banks are covered under the Deposit Insurance and Credit Guarantee Corporation (DICGC) — offering insurance up to ₹5 lakh per depositor.

NBFC deposits, however, do not enjoy such insurance protection.

7. Target Market

Banks generally focus on individual customers, corporates, and government-linked accounts.

NBFCs often target niche or underserved segments such as MSMEs, rural borrowers, vehicle loans, microfinance, and SME financing.

8. Examples

Banks: SBI, HDFC Bank, ICICI Bank, Axis Bank.

NBFCs: Bajaj Finance, Tata Capital, Mahindra Finance, Shriram Finance, Cholamandalam.

Summary Table

Conclusion

Both banks and NBFCs serve as vital pillars of India’s financial landscape. While banks ensure systemic stability and broad financial access, NBFCs bring agility and innovation, especially in high-risk or niche segments. Together, they form the dual engine powering India’s financial inclusion journey.