Unlocking the Indian Enterprise FinTech Revolution: Insights, Themes & Opportunities for 2025 and Beyond

Introduction

India's FinTech transformation has moved well beyond B2C disruptors to an equally powerful evolution in the B2B and Enterprise FinTech space. The convergence of API-led platforms, regulatory push, and digital public infrastructure is creating a robust foundation for enterprise-grade financial innovation. This blog condenses the core insights from the comprehensive "Unlocking Indian Enterprise FinTech" report by Chiratae Ventures and The Digital Fifth, laying out key themes, sectoral opportunities, regulatory catalysts, and startup dynamics that are reshaping India's BFSI infrastructure.

1. The Rise of Enterprise FinTech in India

Initially led by payments and retail credit transformation, the fintech wave is now modernizing internal and customer-facing systems across banks, insurers, asset managers, and NBFCs.

Enterprise FinTechs are now streamlining operations, improving engagement, and automating compliance-heavy workflows.

A clear shift from front-end digital upgrades to middleware and core infra replacement is evident in CBS, loan origination (LOS), and RegTech.

2. Sectoral Landscape and Deep Tech Themes

BankingTech: Surge in modular CBS, CRM upgrades, and BaaS adoption. Small and mid-sized banks are key target customers.

LendingTech: Integrated LOS, LMS, and BRE stacks; focus on co-lending, pre-approved loans, and embedded finance.

PayTech: Cross-border solutions, digital PaaS, and universal payment switches are attracting investment.

WealthTech: Emergence of Wealth-as-a-Service (WaaS) platforms; demand driven by digital-first millennials and embedded wealth.

InsurTech: Insurance-as-a-Service (IaaS), digital onboarding, and underwriting automation gain ground.

RegTech: Data governance, eKYC, AML automation and real-time fraud detection are high-priority areas.

3. Regulatory Backbone and Public Infrastructure

India Stack (Aadhaar, eSign, DigiLocker, AA) enables frictionless verification, lending, and onboarding.

Regulatory bodies (RBI, SEBI, IRDAI) are driving innovation through sandbox frameworks, co-lending rules, and digital lending guidelines.

NPCI initiatives like UPI Credit Line, BBPS, and Tap & Pay are expanding addressable use-cases for FinTechs.

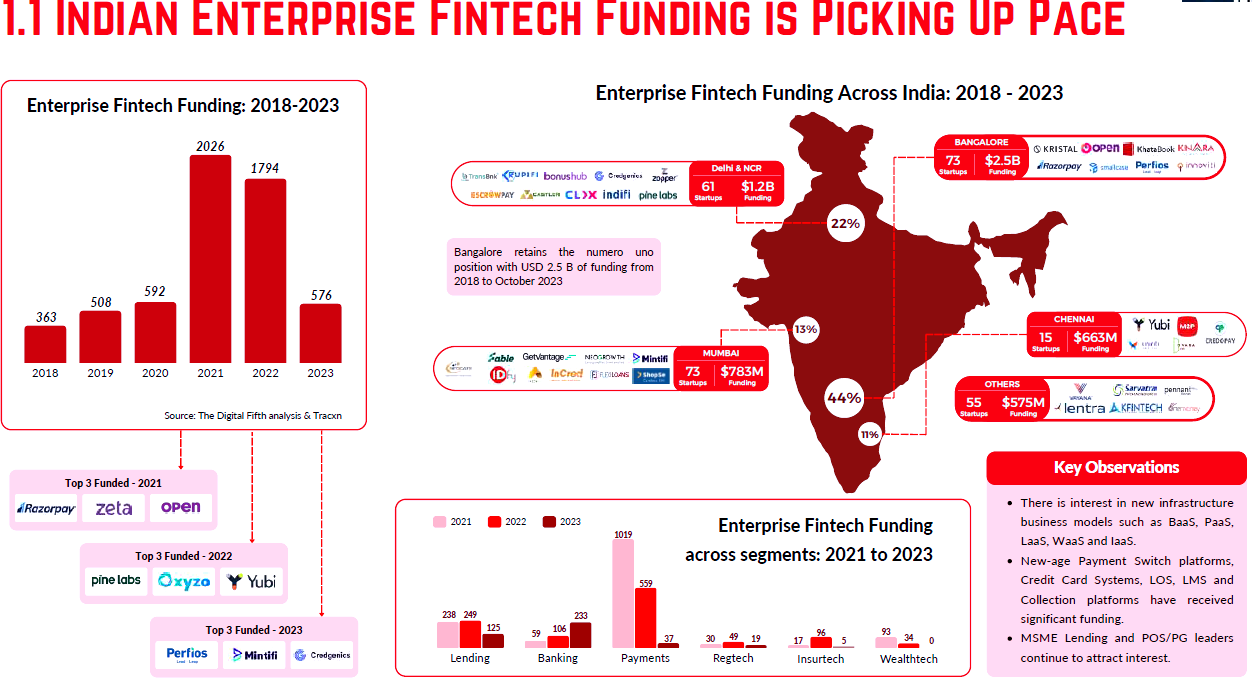

4. Investment Trends and Startup M&A Activity

Enterprise FinTechs saw strong funding between 2021-2023, with LendingTech and BankingTech leading.

Increasing consolidation: PayGlocal, M2P, Yubi, and Perfios acquired complementary startups to build full-stack platforms.

Investors are bullish on horizontal infra (LaaS, BaaS, WaaS), cross-border tech, collections, and cash management tools.

5. Future Outlook: Strategic Focus Areas

CBS modernization and dual-core adoption to support real-time digital banking.

LOS/LMS decoupling and verticalization of Lending-as-a-Service.

Cloud-native architecture and microservices replacing legacy stacks.

ONDC, OCEN, TReDS, and AA creating new distribution rails and data monetization paths.

Rise of white-labeled FinTech stacks, API marketplaces, and SME-first platforms.

Conclusion: A Call to Builders and Backers

India's enterprise-grade FinTech revolution is redefining the financial backbone of its economy. With cloud, APIs, embedded finance, and regulatory clarity accelerating innovation, now is the time for founders, investors, and BFSI incumbents to collaborate and capture the $30B+ opportunity. Whether it's building modular credit engines, vertical SaaS for NBFCs, or RegTech rails for global compliance—Enterprise FinTech is India's next frontier.

Credits: Report by Chiratae Ventures & The Digital Fifth | Analysis.

Full Report : - https://drive.google.com/file/d/1nm0SiIojfjkM5p86nprq2tuWQPl8G9AO/view?usp=drive_link